What Are Section 301 Tariffs?

Section 301 tariffs are additional U.S. import duties imposed on certain products originating from China under the Trade Act of 1974.

Unlike ordinary customs duties, Section 301 tariffs are extra charges layered on top of the base HTS duty rate and are enforced through HTS Chapter 99 provisions.

Since their introduction, Section 301 tariffs have become one of the most common sources of miscalculated import costs.

Why Section 301 Duties Are Often Misunderstood

Many importers assume that the HS code alone determines the duty rate.

In reality, Section 301 applies only when all three conditions are met:

- The product falls under a listed HTS subheading

- The country of origin is China

- The destination is the United States

If applicable, an additional duty — often 7.5% or 25% — must be declared using a Chapter 99 HTS code.

Missing this step can result in:

- Underpaid duties

- Customs audits

- Shipment holds

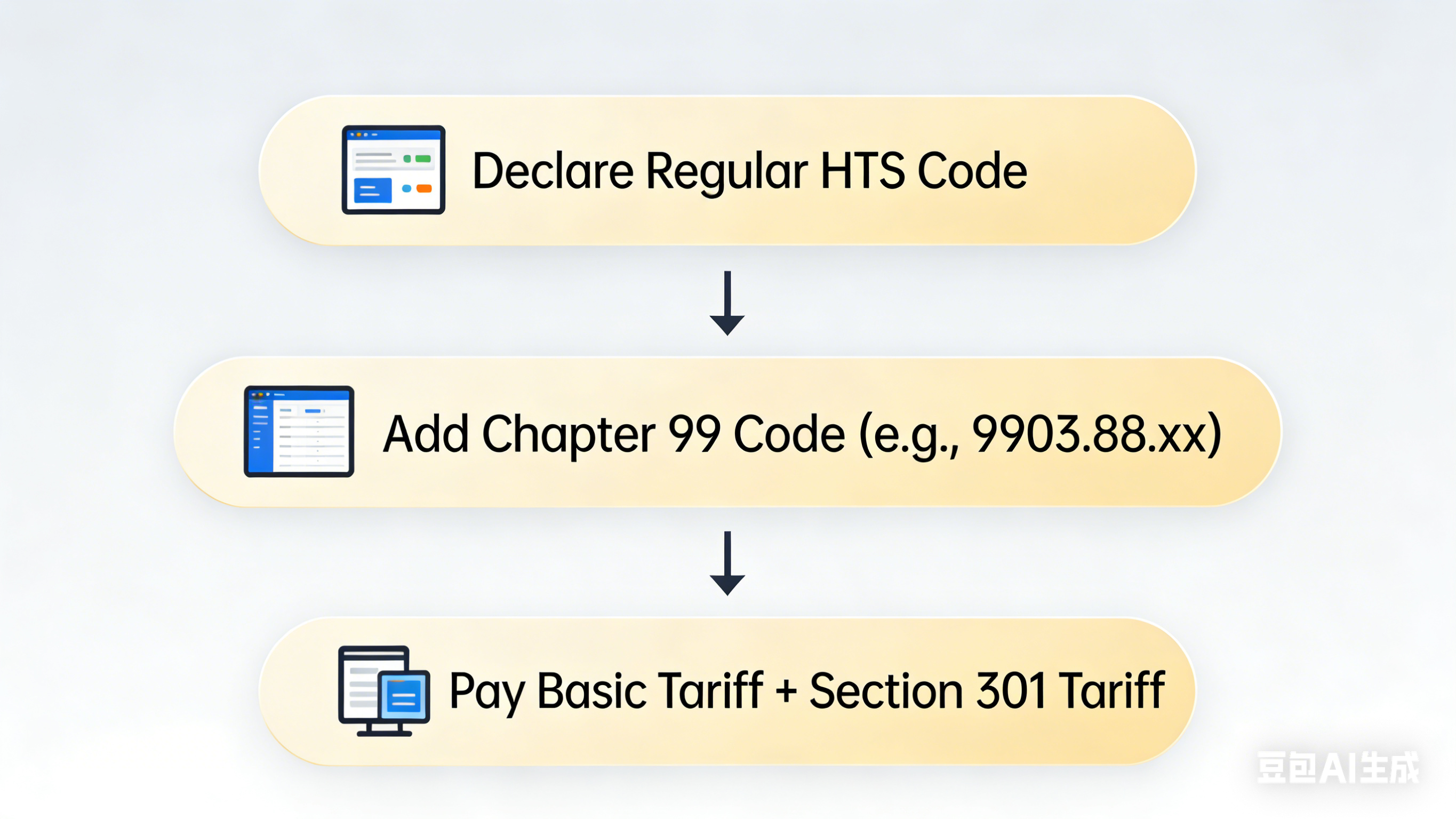

How Section 301 Duties Are Declared

Section 301 duties are not declared under the normal HS code.

Instead, importers must:

- Declare the regular HTS code

- Add the corresponding Chapter 99 code (e.g. 9903.88.xx)

- Pay both the base duty and the Section 301 duty

This is where many calculations break down.

Example: HS 7407.29.16.10 (China → United States)

For HS 7407.29.16.10, the correct duty calculation may include:

- Base customs duty

- Section 301 additional duty

- Chapter 99 HTS reference

- Total effective duty rate

Manually checking this requires multiple tariff tables.

👉 With Fiowind’s Customs Duty Rate Tool, the full Section 301 logic is resolved automatically into a single, clear duty breakdown.

Avoid Section 301 Mistakes with Automated Duty Resolution

Fiowind’s tool:

- Detects Section 301 applicability

- Assigns the correct Chapter 99 code

- Calculates total duty instantly

- Explains why the duty applies

🔗 Check Section 301 duties by HS code:

https://www.fiowind.com/customs-duty-rates